There might be a case in which the alimony payor lives in a state which does tax alimony at the state level, but the recipient lives in a state which does not. In order to indicate that the payor would receive the state tax deduction and the recipient will pay no state income tax on the alimony, you would need to go beyond merely changing the state of residence.

The way to enter this into the FLS would be to specify in the section where alimony is entered whether the alimony is deductible for state tax purposes.

That checkbox controls the deduction of alimony/inclusion of alimony for both parties.

For example, consider a case in which the payor lives in New York and the recipient lives in Connecticut. If the alimony is not includable for Connecticut but is deductible for New York, the thing to do would be to leave the checkbox specifying that alimony is not taxable or includable, and then override the entry in New York.

The place to override it is on the Reports > More Reports > State Taxes report, here:

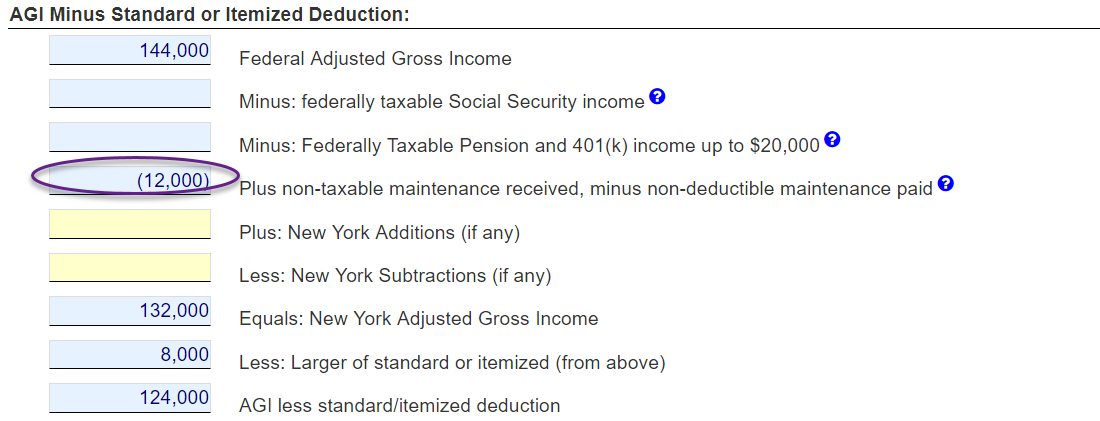

You would override, to enter it as a negative amount.

Each state tax is different, and for many states we do not have that level of detail for the state tax.

In that case, you may just want to make a manual adjustment for the tax impact of the spousal maintenance payment.